How to start a debt management plan without professional help sets the stage for this enthralling narrative, offering readers a glimpse into a story that is rich in detail with casual formal language style and brimming with originality from the outset.

Readers will embark on a journey of financial empowerment as they learn the intricacies of managing debt independently and taking charge of their financial well-being.

Introduction to Debt Management Plan

A debt management plan is a structured repayment plan designed to help individuals or families manage their debts effectively. It involves working with creditors to negotiate lower interest rates, reduce monthly payments, and create a manageable payment schedule.

Importance of Having a Debt Management Plan

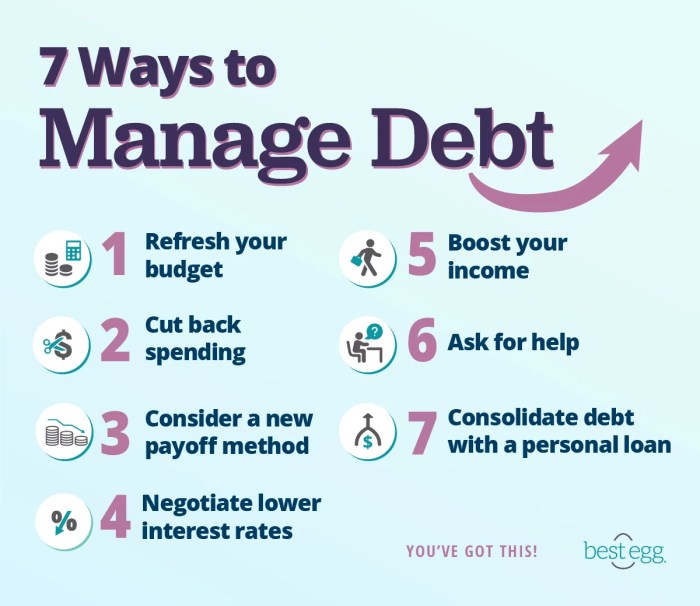

- Provides a clear roadmap for paying off debts

- Helps reduce financial stress and anxiety

- Prevents further damage to credit score

- Allows for better financial planning and budgeting

Benefits of Managing Debt Effectively

- Lower interest rates and fees

- Consolidation of multiple debts into one manageable payment

- Improved credit score over time

- Increased financial stability and peace of mind

Assessing Your Financial Situation

Before starting a debt management plan, it is crucial to assess your current financial situation. This involves identifying all your debts, analyzing your income and expenses, and creating a budget to help you manage your finances effectively.

Identify all your debts and their amounts

- Make a list of all your debts, including credit card balances, loans, and any other outstanding payments.

- Record the total amount owed for each debt to have a clear picture of your overall debt load.

- Include interest rates and minimum monthly payments for each debt to understand the impact on your finances.

Analyze your income and expenses

- Calculate your total monthly income from all sources, such as salary, freelance work, or investments.

- List all your monthly expenses, including rent/mortgage, utilities, groceries, transportation, and other necessary costs.

- Compare your total income to your total expenses to determine if you have any leftover funds to allocate towards debt repayment.

Discuss the importance of creating a budget

Creating a budget is essential for managing your finances effectively and prioritizing debt repayment. By setting limits on your spending and allocating specific amounts towards debt payments, you can stay on track and make progress towards becoming debt-free. A budget also helps you identify areas where you can cut back on expenses and increase your debt repayment efforts.

Negotiating with Creditors

Negotiating with creditors is a crucial step in managing your debt effectively. By communicating with your creditors, you may be able to secure lower interest rates, payment extensions, or reduced payments to make your debt more manageable.

Negotiating Lower Interest Rates

When negotiating lower interest rates with your creditors, it’s important to be honest about your financial situation. Explain why you are struggling to make payments and provide any relevant documentation to support your case. You can also highlight your history of on-time payments and your commitment to settling the debt. Be prepared to negotiate and be persistent in your efforts.

Requesting Payment Extensions or Reduced Payments

If you are unable to make your regular payments, consider requesting payment extensions or reduced payments from your creditors. Contact them as soon as possible to explain your situation and propose a new payment plan that you can afford. Be prepared to provide details about your income, expenses, and any other financial obligations you have.

Strategies for Dealing with Collection Agencies

If your debt has been sent to a collection agency, it’s important to know your rights and how to deal with them effectively. Stay calm and professional when communicating with collection agents, and never provide personal or financial information over the phone. You can negotiate a settlement with the collection agency, but make sure to get any agreements in writing before making any payments.

Creating a Repayment Plan

Creating a repayment plan is a crucial step in managing your debt effectively. This plan will help you organize your finances and work towards becoming debt-free. Let’s explore how to design a personalized repayment plan, prioritize debts for repayment, and methods for tracking progress and staying motivated.

Designing a Personalized Repayment Plan

- Calculate your total debt amount and list all your creditors.

- Determine your monthly income and expenses to understand how much you can allocate towards debt repayment.

- Set realistic goals for paying off your debts, considering your financial situation.

- Explore different repayment strategies such as the snowball method (paying off smallest debts first) or the avalanche method (paying off debts with the highest interest rates first).

- Create a detailed timeline for paying off each debt, taking into account interest rates and minimum payments.

Prioritizing Debts for Repayment

- Focus on paying off high-interest debts first to minimize the amount of interest you accrue.

- Prioritize debts that are in danger of going to collections or have severe consequences for non-payment.

- Consider the emotional and psychological impact of paying off certain debts first to stay motivated.

- Work towards paying off debts that are secured with collateral to avoid losing valuable assets.

Tracking Progress and Staying Motivated

- Regularly monitor your debt balances and payments to see how far you’ve come.

- Celebrate small victories along the way to keep yourself motivated and focused on your financial goals.

- Use visual aids like debt payoff charts or apps to track your progress and stay motivated.

- Seek support from friends, family, or a financial counselor to stay accountable and motivated throughout your debt repayment journey.

Implementing the Plan

When it comes to implementing your debt management plan, consistency is key. It’s crucial to stick to the plan you’ve created in order to effectively tackle your debts and improve your financial situation. Here are some steps to follow and tips to ensure successful implementation:

Follow Your Repayment Plan Consistently

- Make timely payments: Ensure you make your payments on time each month to avoid any late fees or penalties.

- Stick to the allocated budget: Follow the budget Artikeld in your repayment plan to manage your expenses and prioritize debt repayment.

- Monitor your progress: Regularly track your progress and make adjustments as needed to stay on track towards becoming debt-free.

The Importance of Sticking to the Plan

- Build discipline: By sticking to your plan, you develop discipline and financial responsibility that will benefit you in the long run.

- Reduce stress: Consistently following your repayment plan can help reduce financial stress and anxiety associated with debt.

- Improve credit score: Making timely payments and sticking to the plan can positively impact your credit score over time.

Tips for Adjusting the Plan if Needed

- Communicate with creditors: If you encounter financial difficulties, communicate with your creditors to explore possible alternatives or adjustments to your repayment plan.

- Reassess your budget: Periodically review your budget and make adjustments to accommodate any changes in your financial situation.

- Seek professional advice: If you find it challenging to stick to your plan or need guidance, consider seeking help from a financial counselor or advisor.

Managing Financial challenges

Dealing with unexpected expenses and staying out of debt are crucial aspects of managing a debt management plan successfully. It is important to have strategies in place to handle financial challenges effectively.

Handling Unexpected Expenses

- Prepare for emergencies by setting aside a portion of your income each month into an emergency fund.

- Consider getting insurance coverage for major unexpected events like medical emergencies or car repairs.

- Prioritize essential expenses over non-essential ones to ensure you can cover unexpected costs without going further into debt.

- Explore options like personal loans or credit cards with lower interest rates for emergency situations, but use them wisely and pay them off promptly.

Avoiding Falling Back into Debt

- Stick to your budget and avoid unnecessary expenses to prevent overspending.

- Track your spending regularly and adjust your budget as needed to stay on track.

- Avoid using credit cards for non-essential purchases and focus on paying off existing debts first.

- Seek financial counseling or support groups to stay motivated and accountable in your debt management journey.

Importance of Building an Emergency Fund

- An emergency fund acts as a safety net during unexpected financial crises, helping you avoid accumulating more debt.

- Having savings set aside for emergencies reduces financial stress and allows you to focus on repaying debts effectively.

- Start small by setting aside a portion of your income each month and gradually build up your emergency fund over time.

- Having an emergency fund in place provides peace of mind and financial security for you and your family.

Resources and Tools

When it comes to managing debt effectively, having access to the right resources and tools can make a significant difference in your financial journey. From budgeting apps to financial literacy programs, there are various options available to help you navigate through your debt management plan.

Useful Resources for Managing Debt Effectively

- Online debt calculators: These tools can help you estimate your total debt, interest rates, and potential repayment options.

- Credit counseling services: Non-profit organizations offer free or low-cost guidance on managing debt and creating a repayment plan.

- Debt management books: Reading up on personal finance and debt management can provide valuable insights and strategies.

Budgeting Apps or Tools for Tracking Expenses

- Personal finance apps: Apps like Mint, YNAB, and EveryDollar can help you track your expenses, set budgets, and monitor your financial progress.

- Expense trackers: Simple tools like spreadsheets or mobile apps can help you keep a detailed record of your spending habits.

Benefits of Financial Literacy Programs

Financial literacy programs offer a structured approach to improving your understanding of personal finance and money management. These programs can help you:

- Learn the basics of budgeting, saving, and investing.

- Understand the impact of debt on your financial health.

- Gain practical skills to make informed financial decisions.

Conclusion

In conclusion, starting a debt management plan without professional help can be a challenging but rewarding journey towards financial freedom. By following the steps Artikeld in this guide, you can take control of your finances and work towards a debt-free future.

It is crucial to assess your financial situation, negotiate with creditors, create a repayment plan, implement the plan, and manage any financial challenges that may arise along the way. By utilizing the resources and tools available to you, you can navigate through the process successfully.

Importance of Taking Control

- By taking control of your finances, you can regain financial stability and peace of mind.

- Managing your debt effectively can improve your credit score and overall financial health.

- Creating a debt management plan empowers you to make informed financial decisions and work towards your financial goals.

Encouragement for Debt-Free Journey

- Stay committed to your debt management plan and make consistent efforts to stick to your repayment schedule.

- Celebrate small victories along the way to stay motivated and focused on your end goal of becoming debt-free.

- Remember that financial freedom is achievable with determination, discipline, and perseverance.

In conclusion, starting a debt management plan without professional help is a crucial step towards financial freedom. By following the Artikeld steps and staying committed, individuals can pave the way to a debt-free future and secure financial stability.

FAQ Compilation

How can I negotiate lower interest rates with creditors?

To negotiate lower interest rates with creditors, you can reach out to them directly, explain your situation, and highlight your commitment to repaying the debt. It’s essential to be polite and persistent in your communication.

What are some strategies for handling unexpected expenses while on a debt management plan?

To handle unexpected expenses, consider building an emergency fund, cutting back on non-essential expenses, or exploring side income opportunities. Planning ahead and being proactive can help mitigate financial challenges.

Is it necessary to prioritize debts for repayment in a debt management plan?

Prioritizing debts for repayment in a debt management plan is crucial to focus on high-interest debts first and gradually pay off other debts. This strategic approach can save money on interest payments in the long run.